The Complete First Time Home Buyer Guide

First time home buyer needs a complete guide to home buying in order to avoid potentially disastrous mistakes. Fortunately, we’ve sold a few thousand homes and know what to expect! Read through this post to learn how to make great decisions.

The Money is Scary For First Time Home Buyers

Buying your first home is thrilling and scary all at once. You can do everything online- find a home, get an estimate of value, apply for a loan. Simple, right?

But how do you know you are getting the best information? Should you really commit yourself to a 30 year mortgage based on some quick internet research?

Here are some Best Practices every first time home buyer should know.

Don’t Make This Classic First Time Home Buyer Mistake

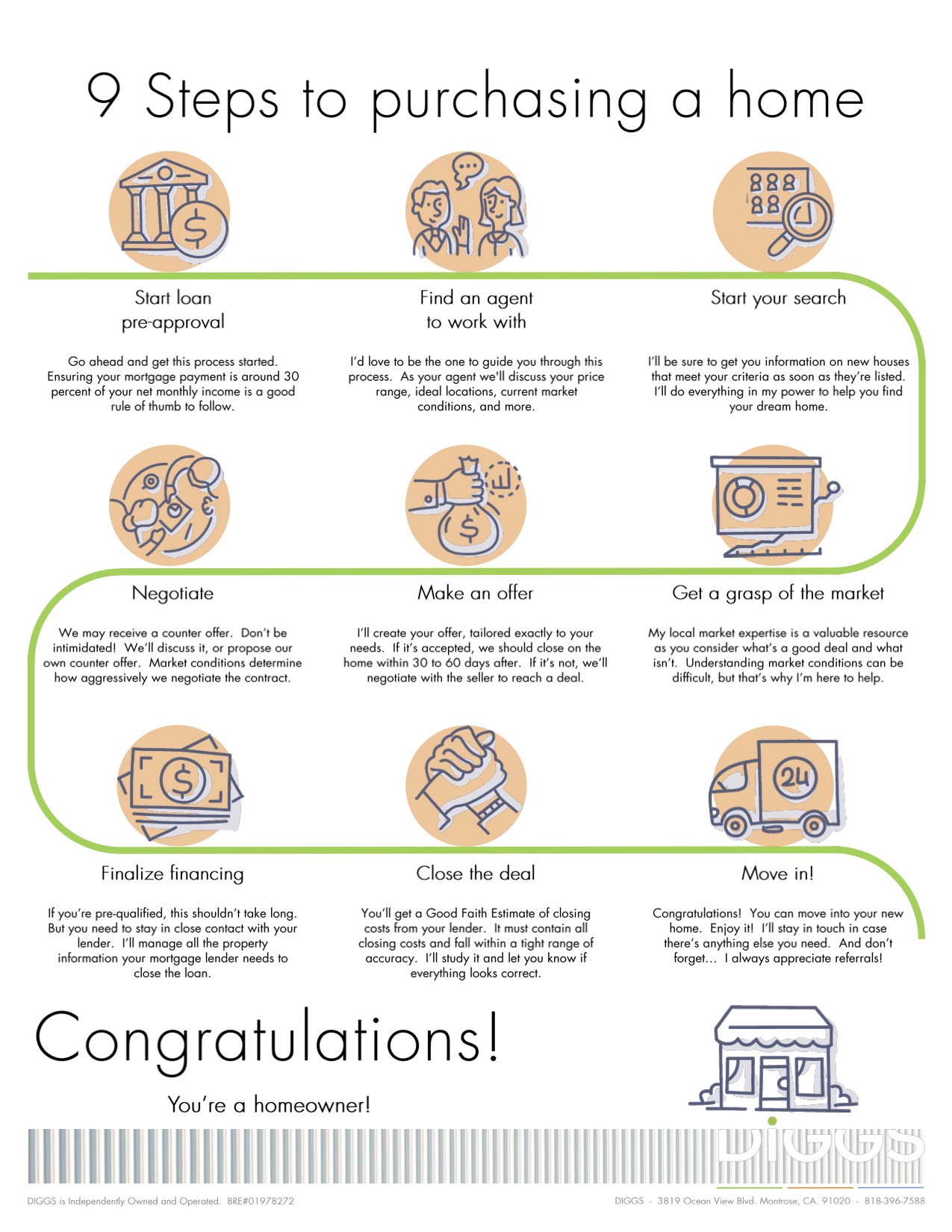

Most homebuyers started looking at homes months before they were ready to buy. There is nothing worse than falling in love with THE house before you are completely ready to buy. Get those finances nailed down before looking any further!

How Much Down Payment Does A First Time Home Buyer Need?

The expected down payment is 20% of the purchase price. That is a hefty amount of money for most first time buyers! It is possible to get a loan with a smaller down payment, but it reduces your chances of getting the home you want. An offer with a low down payment has a higher risk of being denied- and homeowners want the lowest risk possible. In a strong seller’s market high down payment amounts are normal and cash purchases are not unusual.

Now is an excellent time to explore the Bank of Mom and Dad. If an outright gift is out of the question, explore an equity share partnership or a short term loan where you refinance and pay them back after the close of escrow. We know of several cases where parents buy a home for cash and then the children get a normal mortgage after the close to pay the parents back. No matter what you do, be sure to consult with a mortgage professional before transferring any money.

Another option is to check into your retirement savings plan. Under certain circumstances, you can borrow against your plan to obtain cash for a down payment now. The most likely candidate is a 401k Savings Plan, but there are others. Talk to your HR department at work or your personal financial advisor and/or tax advisor.

First Time Home Buyers Need a Loan Pre-Approval

Lots of buyers find the home of their dreams before they get a pre-approval from the bank. And then they lose that house to another buyer. Don’t be that buyer.

Get a pre-approval from a bank or a mortgage broker with an excellent reputation with local real estate agents. Remember the part about how homeowners want low risk? Your pre-approval letter is only as good as the lender behind that statement. A letter from your cousin Guido will not give you a lot of credibility. Local Realtors know who is good… and who isn’t.

Do You Need A Realtor? Who Else Is Going To Watch Your Back?!

We know you can get all the information on the internet. So, why do you need a Realtor?

There is a huge difference between information and knowledge. You are buying a huge financial asset, not a book or bit of clothing. Buying a home without your own trusted advisor is like representing yourself in court or navigating the hedge fund world. Possible, but not advisable.

Think of it this way. You are buying a home for the first time. Everyone in the transaction knows more about buying and selling a home than you do – doesn’t it make sense to have your own, dedicated and experienced advocate?

How Does a First Time Buyer’s Agent Get Paid?

The buyer’s agent is paid by the listing agent as soon as the home is sold. This means you do not pay any commission to your own agent! All the more reason to pick a really good agent to look at for your interests.

The listing broker signed a contract with the homeowner to sell the home. They get a certain percentage of the sales price from the seller and they give a portion of that money to the buyer’s agent. 2.5% of the sales price is a common offer to the buyer’s agents.

Your buyer’s agent does not get to keep all of that money! They give a large portion to their broker (as much as 50%) and they also need to pay expenses- car, E&O insurance, dues, MLS fees, education, marketing, and technology are just the main items. Your agent is likely only getting about 1% of the sales price.

And they only get paid once you successfully buy a home. If you don’t, they don’t.

What Does A Buyer’s Agent Do?

Shopping for a home is very different than the actual buying. Shopping is easy and you are just as likely to spot a potential home as we are. Our real value is in helping you buy the RIGHT home. A local agent can give you the insider’s advantage that can make or break your deal. Our relationships can help make a deal, our experts tell you what you need to know and we know the back story of every comparable sale.

Should I work with the listing agent?

Many first time home buyers assume it’s a good way to go, but it probably not in your best interest. Let me explain. The listing agent will make a lot of money if they represent both you and the seller. That is great incentive to say and do anything to make you buy that particular home and no other. So, who is the agent representing at that point? Certainly not you. No one is looking out for you.

A buyer’s agent is paid when you buy a home. Any home. This means they are better able to help you buy the RIGHT home. See, finding a home is just the beginning. In part four we will talk about all the stuff that can happen along the way.

How do I find a Great Buyer’s Agent?

Most people want an agent who will tell the truth and not “sell me down the river”. They want someone who isn’t trying to just make a buck but is truly looking out for their interests. They want someone to trust. First tIme buyers want this more than anyone!

You deserve a lot more than just a trustworthy agent.

Here are a few factors to consider.

- Local Expert– a local agent has formed good relationships with local listing agents. These relationships can make or break a close deal.

- Experience– Your agent should either have years of personal experience or a true mentor (one that is helping to call every shot, not one that is “on call”). Much chaos and stress can be completely avoided if your agent is experienced.

- Training– negotiation skills are not absorbed, they are taught. Even experienced agents can be terrible negotiators.

- Resources– does the agent have help? Many agents need to it all and that could be to your disadvantage. An agent with a dedicated assistant or team is better able to meet your needs and keep everything running smoothly.

Don’t just go with the first nice Realtor you meet. Interview them. Find out what THEY think they do for a buyer. Come, meet us. We are super clear on what we do for our clients.

How Do You Know It’s The Right House?

You know what you want. As a first time buyer you just need to find out if you can afford it. That is where the internet really helps out. You can find out, anonymously, whether your dreams are affordable or unrealistic. You can also see where your dream homes might be affordable. Are you willing to do the commute?

Shopping for your first home

While the internet makes shopping super easy, it can also be frustrating. The information is not always accurate and your dream home might not be available for sale- even though it looks like it is! Zillow/Trulia (owned by the same people) is the most popular, but it is also the least accurate. Many homes are simply not available to buy. When you are done window shopping and are ready to buy you need to make a change.

The right agent is invaluable

In this fast-paced market you need two things. First, you need a top buyer’s agent who is actively and aggressively searching for your ideal home. A top buyer’s agent spends most of their time previewing new listings on the market and networking with other agents to get the inside scoop on homes not quite on the market.

Tech makes it easier for first-time buyers to find the right home

The second thing you need is great technology. You want an intelligent tool that makes searching faster and easier. You don’t want to know about every 3 bedroom home in your price range in Glendale, right? But you do want to know about every Spanish style home with an open concept kitchen. Our technology can “read” pictures and deliver just the right homes to your inbox.

Hate scrolling through 52 photos to see what the kitchen looks like? Our app lets you click “kitchen” and get right to the kitchen pictures. Have you ever wanted to compare just the kitchens of your top choices? Or, perhaps, compare the bathrooms? Our side by side comparison tool is just the ticket.

Have you ever wanted to compare just the kitchens of your top choices? Or, perhaps, compare the bathrooms? Our side by side comparison tool is just the ticket.

First Time Buyers Have A Lot Of Questions

Lastly, you want to get answers about specific homes right away. You can text your agent, right from the app, and your agent will not only get the text but have full access to the home you are seeing. Communication and answers are quick and easy!

DIGGS has unique tools to help the first time buyer

Right now, DIGGS is the only place to get these tools. We make sure that we have the top buyer’s agents and with the very best tools for their clients. Contact us to find out how you can become a DIGGS client – we are you guides to buy a Glendale CA home.

First Time Buyer Negotiations and Escrow

Finding your dream Glendale Ca home is just the start. Now you need to make an offer and pray that it is accepted.

Multiple Offers

When more than one offer is being considered at the same time it is called a multiple offer situation. This is normal in today’s market and the smart buyer is prepared. While uncomfortable for most buyers, it is not automatically bad.

It is only bad if you are unprepared and get swept up in an emotional bidding mentality. A great agent will stop you from going there. A great agent will help you see exactly where this house ranks considering your personal priorities, budget, and timing needs. They will help you craft a bid that has the highest likelihood of being accepted but is still within your means.

Offers and Counter Offers

Once the seller reviews all the offers they can choose to accept, reject, or counter each offer. They can also counter-offer more than one offer. They can counteroffer on price as well as terms. You can then counter the counteroffer. This can go on forever, but typically the seller will decide on this first counter offer.

Counteroffer strategy is worth an entire blog post on its own. An experienced and skilled negotiator is worth her weight in gold at this point, alone.

Open Escrow

Once your offer is accepted the fun truly begins! There are three main contingencies- if you can’t remove these contingencies on time you might not buy the home and your deposit will be returned.

Inspection Contingency– you get to research and inspect this home as much as you need. The one major rule is you can’t destroy anything in order to examine. If you discover something you don’t like you can either ask the seller to fix it or give credit or you can walk away.

Appraisal Contingency– your lender will send an appraiser to inspect and measure the house. Then the appraiser will study recently sold homes to produce an appraisal opinion. If that opinion is below the sales price the bank might not loan you enough money to buy the home. You can walk away. (It is worth noting that there are many situations where the home does not appraise and it is in your best interest to buy the home anyway. Another blog post for another day!)

Loan Contingency– This last contingency is actually the smallest hurdle. Normal buyers with normal finances typically receive final loan approval, although the timing of the approval varies depending on the lender. However, if you are denied loan approval, you can walk away.

Closing Escrow

Congratulations, you’ve crossed the finish line! In Glendale, Ca your physical appearance is unnecessary to the closing process. It is different in other states.

A day or two before the scheduled close you wired the last of your down payment into escrow. On closing day the title representative records your name as the new owner of the property and calls escrow with the happy news. This can happen at any time of the day from 8:30 am to 4:00 PM. Once we get the call we can arrange to give you the keys to your new home!

Homeownership

Congratulations! You now own a home. Are you elated? A little unsure, perhaps?

Don’t worry, the daily mechanics aren’t too far from life as a renter. But, there are a few critical differences, so let’s get you set up for your happily ever after.

Your Neighbors – you’ve made a pretty significant investment in this home. You can’t just up and leave because your neighbors don’t share your taste in music. Make a little effort to introduce yourself. At a minimum, smile and say hello when you see your new neighbors on the street. Remember, they are just as concerned about you as you are about them. Don’t let your first interaction be a complaint on either side.

Your Taxes – Congratulations! You now qualify for the largest tax deduction possible for most US Citizens, the Mortgage Interest Deduction. Most first time home buyer’s will wait for their first tax return to realize the financial benefit of that deduction. Be proactive. Meet with your tax account or financial advisor now and arrange for your employer to deduct less tax from each paycheck.

Repairs – The landlord is no longer the person you call when something breaks. And, something will break within the first week or two. It’s like your house is testing the new owner. You should have received a one year Home Warranty policy when you purchased. We negotiate this for all DIGGS buyers. Your home warranty company is your first phone call and they will arrange to send a service professional to fix or replace the item. If you call the plumber, first, the home warranty will not cover the bill.

Services- Are you inspired to make changes you would not have made as a renter? Do you want to paint? Install landscape, maybe even do some remodeling? This is normal, but you might be lost as to who to call. That’s why we pulled all of our favorite vendors and service professionals together into the DIGGSVendors.com guide. Each vendor is either our personal service pro or was recommended by a member of our DIGGS Tribe.

Estate Planning – You are a homeowner, and this means you qualify as a bonafide adult. Adults have estate plans in order to control their financial wealth after their death. That means you. So- have you met with an estate planner yet? At a minimum, you should consider putting your new home into a living trust. Should the unexpected happen, your heirs will have a significantly easier time handling your estate if you do.

Important Reading: Check out our Ultimate Home Buyer Guide for the best local advice on home buying.